How Working Capital Actually Gets Set in a Business Sale

How Working Capital Actually Gets Set in a Business Sale

A common instinct before a sale is to clean up the balance sheet. Collect the receivables, stretch the payables, run down inventory. It feels productive. It is not how this works.

I have written elsewhere that the price is not the proceeds. Working capital is one of the reasons why. It catches owners off guard, especially in seasonal businesses, and it is one of the biggest preventable surprises in what an owner takes home.

What Working Capital Means in a Sale

Most transactions transfer the business with what the parties agree is an appropriate level of working capital. Working capital is the receivables, inventory, prepaid expenses, and other current assets a business needs to operate, less the current obligations like accounts payable and accrued expenses. The convention you will hear is "cash-free, debt-free with a normalized level of working capital." Three pieces matter in that phrase.

Working capital excludes cash. You keep the cash. Working capital excludes debt. You retire the debt at closing. What transfers is what the business needs to keep running the day after you hand over the keys: enough inventory on the shelf, enough receivables in the pipeline, less the bills coming due.

The buyer is paying for a business that can keep running normally from day one, not one that requires an immediate cash infusion to keep the lights on.

Why It Looks Different in Every Business

The size and shape of that requirement depends on the business:

- A B2B distributor on net-30 to net-60 terms carries significant receivables and warehouse inventory, often equal to several months of revenue at any given moment.

- A consumer retailer with card-based payments and fast inventory turns runs mostly on cash, with much smaller working capital needs relative to revenue.

- A government contractor may wait 30 to 60 days for payment, which inflates receivables on the balance sheet even for a healthy business.

- A services business without product inventory is leaner still, with working capital concentrated in unbilled work and receivables.

There are also industries where inventory is carved out of working capital. Where inventory value is highly volatile, represents a large share of total business value, or requires specific appraisal, it is typically priced as a separate line item in the purchase agreement, at cost or by appraisal. Jewelry stores and car dealerships are the obvious examples. Treating that inventory inside a 12 to 24 month trailing average would distort the deal for both sides.

Fast-growing businesses also get a different treatment. A 12 to 24 month average will lag the current need, because a business growing 25 or 30 percent a year needs more working capital next quarter than it had this quarter. Two methods are common:

- Shorten the trailing window, often to three or six months, so the peg reflects the current run rate rather than where the business was a year ago.

- Express the peg as a percentage of trailing revenue, so the requirement scales with the top line as the business grows.

Either method results in a higher peg.

Working capital is not one number across businesses. Where your peg lands depends on the kind of business you run.

How Seasonality Changes the Math

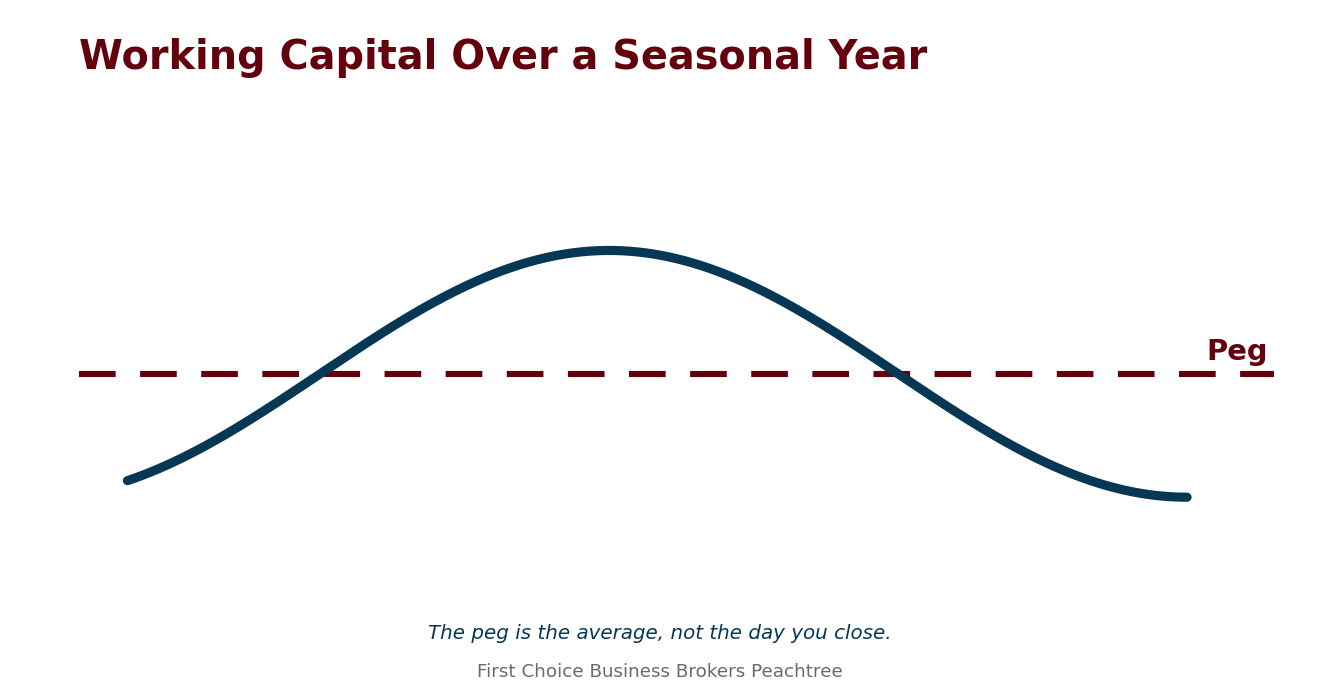

For a seasonal business (e.g., building products, construction, certain manufacturing, agribusiness), working capital moves in a cycle, not a line. Inventory and receivables swell during the spring and summer selling season, then recede through fall and early winter before climbing again. The cycle repeats every year.

If the requirement were measured on the day of closing, the number would swing with the calendar. A business closing in June would look very different from the same business closing in December, even though nothing structural had changed. So it is not measured that way. The peg is set on an average of the trailing 12 to 24 months, which strips out the seasonal noise and gets at what the business needs to operate.

I have walked owners of seasonal businesses through this many times. It usually takes some explaining and a few questions back and forth. Most arrive at the same conclusion: the trailing average is fair to both sides, because it protects the owner from being penalized for closing in a trough as much as it protects the buyer from overpaying at a peak.

The Peg Is a Negotiation, Not a Formula

The peg is a negotiation, not a formula. Where the trailing window starts, how outlier months are treated, which line items count toward working capital and which sit outside it, all get negotiated in the broader context of the deal. A buyer with a sharp advisor will push for definitions that benefit them. An owner with a sharp advisor will push back.

Timing matters, sometimes as much as definitions. Setting the peg upfront, alongside the purchase price, while you still have alternatives and the buyer is competing for the deal, is one conversation. Letting it drift into confirmatory diligence, when the owner has fewer alternatives, is a very different one. Both sides know this. Sellers push to settle the peg early, when their leverage is at its highest. Buyers push to delay, often by pointing to their outside accountants still running confirmatory diligence on the financials. That is a legitimate process, but buyers use it to extend the timeline, because the leverage shifts toward them the longer the deal runs. Same number, different outcome.

This is why preparation matters. A Quality of Earnings analysis done before going to market does several things at once:

- It independently verifies the quality of the reported earnings.

- It surfaces normalizing adjustments and one-time items.

- It identifies the working capital trend and frames the appropriate trailing window.

- It gives the owner the analytic foundation to negotiate the peg early, when leverage is at its highest, rather than reacting to it later.

The buyer's accountants are going to do their own confirmatory work on the numbers either way. Lead with your working capital analysis, or defend against someone else's.

The trailing average also does something useful for both sides: it resists short-term gaming. Running receivables down, stretching payables, or drawing down inventory in the weeks before closing does not meaningfully move a 12 to 24 month trailing average. A month or two of distortion gets diluted across the broader cycle.

Why Late Cleanup Fails

Buyers also notice. A balance sheet that shifts noticeably in the months before closing is obvious to a sophisticated buyer. The math may not move, but trust does.

The peg is not a snapshot of closing day. It is an average of what the business has needed to operate over a real cycle. The closing-day delivery is then measured against that peg.

That keeps both sides honest. The buyer cannot demand an unrealistic level of working capital. The owner cannot strip the business in the weeks before closing without consequence. The reference point is fixed, and it is fair.

A Concrete Example

Picture a business with a working capital peg of $1 million. At closing, the actual working capital on the balance sheet is $800,000. The buyer adjusts the closing wire down by the $200,000 shortfall, the gap they have to fund to keep the business running. That is not a price renegotiation. It is a mechanical adjustment built into the purchase agreement, applied at closing.

The math runs the other direction too. Deliver $1.2 million against the same peg, and the wire moves up by $200,000 in the owner's favor. The mechanism is symmetric. Neither direction is a windfall. Whichever way the adjustment runs, it is a transfer of working capital that someone has to fund.

The Real Lever Is How You Run the Business

Here is what actually moves the number. You cannot trick the working capital requirement, but you can lower it honestly. A business that collects faster, turns inventory more efficiently, and manages its terms with discipline needs less working capital to run.

That is real money. Not at the closing table, where the lower peg means a lower amount transferred, but every month you own the business. Less cash and credit tied up in receivables and inventory means more available for distributions, debt paydown, growth investment, or weathering a slow quarter without drawing on a line of credit. That value compounds quietly across years of ownership.

There is a second benefit that belongs in the positioning story. A business that demonstrates disciplined working capital management tells a better story to a buyer. It signals quality in the people, processes, and systems that will endure after the transaction. That kind of signal tends to support better terms, broader interest, and a stronger negotiating position when the time to sell does come.

It is not a maneuver you execute in the last 90 days. It is a way of running the business that compounds over years.

Working capital is not something you clean up before a sale. It is a discipline you build long before one.

Honest valuation. Disciplined process. Confidential execution.